The Enduring Logic of Austerity

Austerity won't collapse under its own contradictions. We'll need a movement for that.

The European Central Bank in Frankfurt, Germany. Chris Goldberg / Flickr

It has gradually entered our awareness that the Greek trade account is now balanced. Greece no longer depends on financial markets (or official transfers, or remittances from workers abroad) to finance its imports. This is obviously important for negotiations with the “institutions,” or at least it ought to be.

I was wondering, how general is this shift is toward a positive trade balance? Martin Wolf recently pointed out in the Financial Times that over the past five years, the euro area as a whole has shifted from modest trade deficits to substantial trade surpluses, equal to 3 percent of euro-area GDP in 2013. He does not break it down by country, though. I decided to do that.

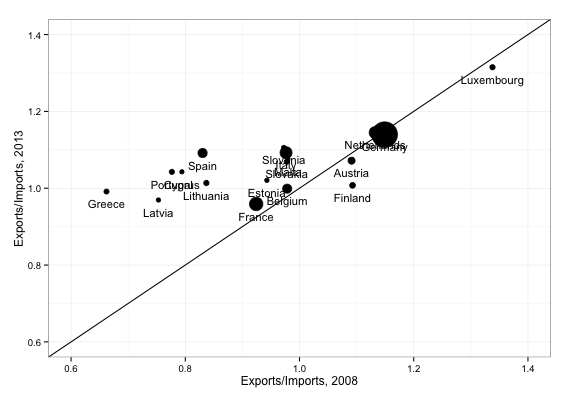

|

| Euro area trade ratios, 2008 and 2013. The size of the dots is proportional to total 2008 trade. |

Here, from Eurostat, are the export-import ratios for the euro countries in 2008 and 2013. Values greater than one on the horizontal axis represent a trade surplus in 2008; only a few northern European countries fall in that group. Meanwhile, in seven countries imports exceeded exports by 10 percent or more.

By 2013, the large majority of the euro area is in surplus, while not a single country has an excess of imports over exports of more than 5 percent. The distance above the diagonal line indicates the improvement from 2008 to 2013; this is positive for every euro-area country except Austria, Finland, and Luxembourg, and the biggest improvements are in the countries with the worst ratios in 2008. The surplus countries, apart from Finland, more or less maintained their surpluses; but the deficit countries all more or less eliminated their deficits.

So does this mean that austerity works? Yes and no. It is certainly true that Europe’s deficit countries have all achieved positive trade balances in the past few years, even including countries like Greece whose trade deficits long predated the euro. On the other hand, it’s also almost certainly true that this has more to do with the falls in domestic demand rather than any increase in competitiveness.

This is shown in the second figure, which gives the ratio of 2013 imports to 2008 exports on the vertical axis, and 2013 exports to 2008 imports on the horizontal axis. (This is in nominal euros.) Here a point on the diagonal line equals an equal growth rate of imports and exports.

Most countries are clustered around 15 percent growth in imports and exports; these are the countries that had balanced trade or surpluses in 2008, and whose trade ratios have not changed much in the past five years. Only one country, Estonia, has export growth substantially above the European average.

But all the former deficit countries have import growth much lower than average. (As indicated by their position to the left of the main cluster.) It’s evident from this diagram that the move toward balanced trade in the deficit countries is about throttling back imports, not boosting exports. This suggests that it has more to do with slow income growth than with lower costs.

|

| Again, the sizes of the dots are proportional to 2008 trade volumes. |

Still, the fact remains, trade deficits have almost been eliminated in the euro area. Liberal critics of the European establishment often say “not every country in Europe can be a net exporter” as if that were a truism. But it’s not even true, not in principle and evidently not in practice. It turns out it is quite possible for every country in the euro to run a trade surplus.

The next question is, with whom has the euro area’s trade balance improved? Europe outside the euro, to begin with. The country with the biggest single increase in net imports from the euro zone is, surprisingly, Switzerland, whose deficit with the euro area has increased by close to 60 billion. Switzerland’s annual trade deficit with the euro area is now 75 billion, about a quarter of the area’s overall trade surplus.

Norway and Turkey have increased their deficits by about 15 billion each. The rest of the increase in net exports are accounted for by increased surpluses with Africa (26 billion), the US (27 billion), and Latin America (35 billion, about half to Brazil), and a decreased deficit with Asia (135 billion, including a 55 billion smaller deficit with China, 30 billion smaller with Japan and 20 billion with Korea). Net exports to Australia have also increased by 10 billion.

Why do I bring this up? One, I haven’t seen it discussed much, and it is interesting.

But more importantly, the lesson of the Europe-wide shift toward trade surpluses is that austerity can succeed on its own terms. I think there’s a tendency for liberal critics of austerity to assume that the people on the other side are just confused, or blinkered by ideology, and that there’s something incoherent or self-contradictory about competitiveness as a Europe-wide organizing principle. There’s a hope, I think, that economic logic will eventually compel policymakers to do what’s right for everyone.

Personally, I don’t think that the masters of the euro care too much about the outcome of the struggle for competitiveness; it’s the struggle itself — and the constraints it imposes on public and private choices — that matters. But insofar as the test of the success of austerity is the trade balance, I suspect austerity can succeed indefinitely.